ASSIGNMENT3字数1900

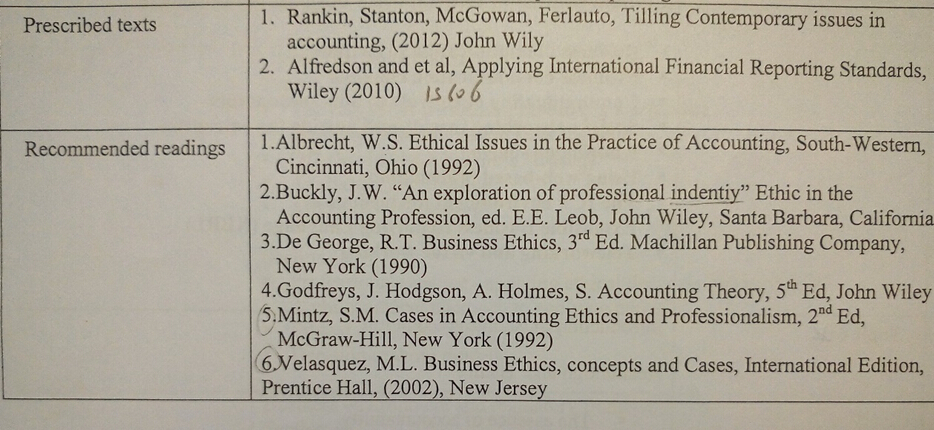

参考书目

Introduction介绍

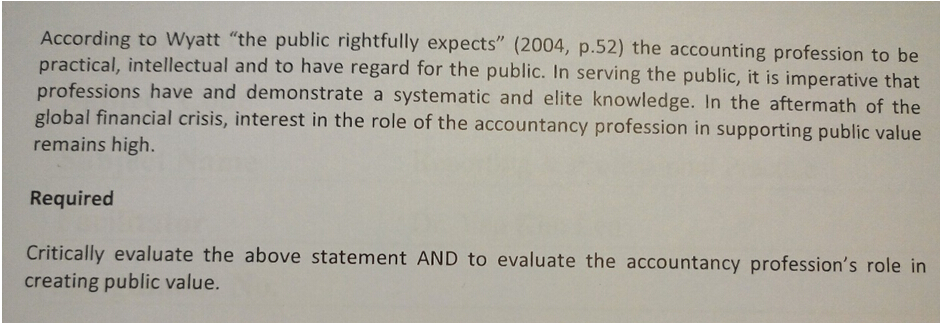

职业道德是指人们在职业生涯中所遵循的基本道德准则。即,在职业生活中所体现的一般社会道德。职业道德是职业道德,结合职业纪律、职业能力和职业责任(情人节,Fleischman贝特曼,2015)。它属于自律范畴,通过公约、法典等对职业生活的某些方面进行规制。职业道德既是参与者的行为准则,又是公众的期望,是社会参与者的道德规范和责任。会计作为最古老的职业之一,会计师已经发展了自己的伦理,会计伦理。会计职业道德是专业的和日常生活中适用于会计师职业道德的标准,突出了会计师的专业特征,协调了会计师在日常生活中的专业和经济关系(巴登,2014)。它是会计工作中普遍存在的公共道德,它制约着参与者的行为,调整了会计与社会之间的社会规范和社会关系,以及会计人员与各种利益集团之间的关系。Professional ethics refers to the basic moral to be followed in people’s professional life. Namely, the general social morality embodied in professional life. The term of professional ethics is the combination of professional morality, professional discipline, professional competence and professional responsibility (Valentine, Fleischman& Bateman, 2015). It belongs to the scope of self-regulation, which regulates on some aspects of professional life through conventions, codes and so on. Professional ethics is both the conduct guidelines of participator and expects of the public, and moral norms and responsibility of participator to the public. As one of the most ancient professions, accountancy has developed its own ethics, accounting ethics. Accounting ethics is the professional ethics applies to accountants during their professional and daily life, which highlights the professional features of accountants, coordinates the professional and economic relationship in accountants’ professional and daily life (BADEN, 2014). It is the general public morality embodied in accounting work, guidance, which restricts participator’s behavior, adjusts social norms and social relationships between the accountants and society and the relationship between accountants and various interest groups. It runs throughout all areas of accounting work and reflects the integration of social development and personal characteristic development. It also relies on interpersonal relationship adjustment that if it is reasonable, or consistent with the morality requirements and rightfully expects of the society. It transfers the outside, meaning the society, requirements and expects to a internal non-mandatory specification to accountants (Martinov-Bennie&Mladenovic, 2015). Therefore, accounting profession should be practical, intellectual and have regard for the public. In serving the public, it is imperative that professions have and demonstrate a systematic and elite knowledge. it is consistent with the accounting ethics. It will give a brief introduction of accounting ethics and the importance of accounting ethics in the aftermath of the global financial crisis, since interest in the role of accountancy profession in supporting public value remains high.

Accounting ethics and public value

Accounting ethics in the aftermath of global financial crisis

Conclusion

In conclusion, accounting profession should be practical, intellectual and have regard for the public. In serving the public, it is imperative that professions have and demonstrate a systematic and elite knowledge. it is consistent with the accounting ethics. It will give a brief introduction of accounting ethics and the importance of accounting ethics in the aftermath of the global financial crisis, since interest in the role of accountancy profession in supporting public value remains high.

References